Institutional Insights: JPMorgan Flows & Liquidity 2/4/26

Market Flow Overview

1. US Liquidity & Asset Redeployment: $380bn YTD cash balances (annualized $1.8tr). Potential $4.5tr could flow into equities, bonds, and gold if Middle East tensions ease.

2. De-Dollarization in FX Reserves: Central banks increased gold reserves to record highs while reducing dollar holdings, with $20bn net FX inflows in Q4'25 despite $50bn in dollar outflows.

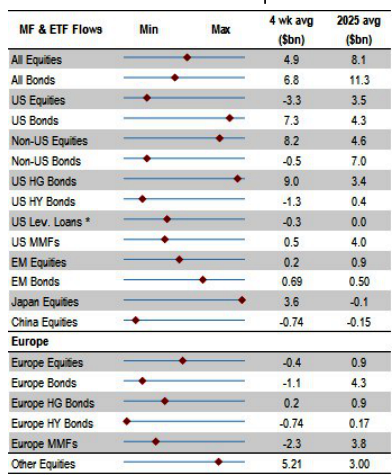

3. Equity ETF Flows: March outflows were offset by subsequent inflows, showing no sustained retail "buy-the-dip" trend. US equity ETFs led regional inflows.

4. Leveraged ETF Impact: March saw $28bn in negative rebalancing flows, amplifying market movements. Excluding this, net equity fund buying reached $68bn.

5. Institutional-Driven Correction: Market corrections linked to institutional activity, with equity exposure at 60% (down from January's 80% peak).

6. Geopolitical Cash Shifts: Middle East tensions led to institutional cash buildup, with potential normalization into equities, bonds, and gold if the Strait of Hormuz reopens.

7. Crypto & Gold Trends: Q1'26 crypto flows slowed to $11bn (annualized $44bn), while central banks’ gold reserves rose to 31% of total reserves by Q1'26.

8. Speculative Positioning: Natural gas futures saw significant speculative interest post-Middle East conflict, outpacing crude oil.

9. S&P500 Sentiment: Bullish sentiment remains high (>75%), but institutional flows show a strong negative correlation with S&P500 upside potential.

10. Skew & Positioning: Bearish signals in S&P500 and iTraxx Main skews; bullish demand for German Bunds and gold. Equity vs. UST futures positioning indicates net long equities over bonds.

11. Bond Market Trends: High-grade ex-EM bonds saw strong inflows, signaling a preference for safer assets. Bond beta volatility spiked, reflecting heightened risk sensitivity.

12. Short Interest Decline: SPY and QQQ short interest fell, suggesting reduced bearish bets and possible bullish momentum.

13. Crypto VC & Bitcoin Strategy: Crypto VC funding remains robust, focused on infrastructure and stablecoins, though deal counts declined. MicroStrategy continues Bitcoin accumulation via equity issuance.

14. Market Signals: Negative momentum in 10Y UST indicates caution; risky currency spreads suggest risk-on sentiment. Equity health metrics point to a stable S&P500 outlook.

15. Key Drivers: Institutional flows, economic momentum, and turnover are significant predictors of S&P500 trends.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!