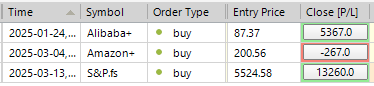

SP500 LDN TRADING UPDATE 17/03/25

SP500 LDN TRADING UPDATE 17/03/25

WEEKLY BULL BEAR ZONE 5690/5700

WEEKLY RANGE RES 5768 SUP 5488

DAILY BULL BEAR ZONE 5560/50

DAILY RANGE RES 5671 SUP 5586

WEEKLY ACTION AREA VIDEO TO FOLLOW AHEAD OF NY OPEN

GOLDMAN SACHS TRADING DESK VIEWS

U.S. EQUITIES SUMMARY: Weekly Recap

FICC and Equities | 14 March 2025 |

It was a challenging, macro-driven week for U.S. equities, with the market stuck in a defensive posture as investors tested the "pain point" for policy. While the "Trump Put" appears to have been re-struck at lower levels, oversold conditions persist across sectors. Although the worst of the damage seems to be behind us, the market remains without a clear catalyst, weighed down by lingering "scar tissue" from recent selloffs.

Weekly Performance

- SPX: -2.3% (Equal Weight: -2.3%)

- NDX: -2.5%

- RTY: -1.8%

- 10-Year Yields: +21 bps to 4.31%

Momentum indicators (GSP1MOMO) and Hedge Fund VIP vs. Most Short (GSPRHVMS) rebounded ~400 bps. Sector performance was mixed:

- Best Performers: China ADRs, Defense, Infrastructure

- Worst Performers: Middle-income Consumer, Retail, Meme Stocks, Obesity Drugs

Flows Overview

Long-only (LO) funds and hedge funds (HFs) were net sellers, with LOs offloading $7 billion and HFs shedding $1 billion. Flows were characterized as "methodical LO supply," with selling concentrated in Semiconductors, Financials, and Industrials. However, Friday saw renewed demand for TMT (Technology, Media, Telecom) as indices stabilized.

Over the past three weeks, LOs have sold more than $15 billion in U.S. equities, marking the second-largest 15-day net sell skew in three years. Notably, LO cash as a percentage of total assets was at 20-year lows entering the quarter.

On the HF side, significant de-grossing occurred last Friday and Monday, marking the largest two-day de-grossing period in four years. However, U.S. equities were fully re-grossed in the following three sessions (Tuesday-Thursday), even as other regions saw continued de-grossing.

Prime Brokerage Insights

Global equities were net sold for the fourth consecutive week, driven by both long and short sales (1.5 to 1 ratio). Single stocks and macro products were net sold, with single-stock selling hitting its highest level since August 2024.

Positioning and Performance

- Fundamental Long/Short (L/S):

- Gross leverage decreased 2.0 points to 198.1% (85th percentile, 1-year).

- Net leverage dropped 1.9 points to 52.7% (1st percentile, 1-year).

- Performance fell -1.57%, driven by beta losses (-1.92%) partially offset by long-side alpha gains (+0.35%).

- Systematic L/S:

- Performance rose +0.99%, driven by alpha gains (+1.16%) on the long side, partially offset by beta losses (-0.17%).

Volatility dropped significantly today, rounding off a hectic week. UX1 lagged the spot move by approximately 1.5v, while fixed strike volatility adjusted lower across the curve. Trading activity was relatively subdued during the rally, but notable interest emerged in Chinese upside plays. Over 200,000 ASHR April 30 calls traded today, alongside similar upside buying in FCX, ahead of key Chinese economic data and a busy earnings week for the CSI300. Dealer gamma remains neutral but shortens on the upside, further amplifying price action. Looking ahead, next week features the March FOMC meeting in the U.S., with the straddle for the week pricing in a 2.25% move.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 71% and 74% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!