Institutional Insights: Credit Agricole FX Weekly 10/01/25

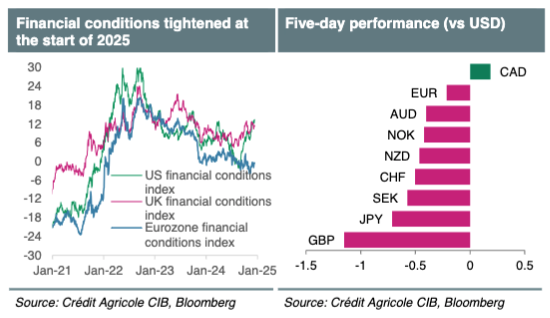

At the beginning of 2025, market risk sentiment experienced a significant decline, influenced partly by a marked tightening of global financial conditions due to rising government bond yields. These yields appear to be driven by investors' concerns regarding the effects of persistent inflation and a potential growing mismatch between bond supply and demand in the future.

These worries have overshadowed ongoing concerns about the robustness of the global economy.

The recent market trends have enhanced the attractiveness of the high-yielding, safe-haven King USD, which could support the currency in the short term, as the tightening of global financial conditions is partly a result of a reassessment of the market's dovish outlook on the Fed, influenced by: (1) persistent US inflation and the resilient US real economy recently; and (2) the increasing risk of another US-led global trade conflict and its implications for global inflation and growth in the upcoming months.

Conversely, the GBP has become the largest loser in the G10 FX market since the year's onset. This is due to the fact that, in the UK, soaring gilt yields have exacerbated market concerns that a weakening economy could undermine the Labour government's budget plans, necessitating new fiscal austerity measures in the spring. Consequently, the GBP may continue to serve as the preferred outlet for many anxious investors worried about the prospects of their UK investments.

In the short term, alongside the resilience of global risk sentiment, FX investors may pay close attention to today's Non-farm payrolls and next week's CPI and retail sales data. Many positive factors are already reflected in the USD price, and we believe that it would require positive data surprises to extend the overbought and overvalued USD's upward trend.

Additionally, next week's UK GDP, CPI, and retail sales data may draw significant attention leading up to the BoE's February policy meeting. Given the recent aggressive movements in the FX market, any potential positive data surprises could assist the struggling GBP in stabilizing. The latest labor market data from Australia may also be a point of interest.

We have revised our outlook for the EUR/USD following the US election, but we believe that many negative factors are already reflected in the price, and the pair appears to be oversold and undervalued. Our economists do not foresee a recession in the Eurozone and anticipate a terminal ECB rate of 2.25%, which is significantly higher than current market expectations for European rates. Additionally, while recent political events in France and Germany have unsettled EUR investors, our rate strategists are not positioned for a repeat of the sovereign debt crisis from a decade ago and believe that many negatives are already accounted for in the pricing. Moreover, we think that a potential reduction or even withdrawal of US support for Ukraine under President-elect Donald Trump could ultimately lead to the end of the war by 2025. This development could ease geopolitical risks in Europe, potentially boosting domestic demand in the Eurozone. An end to the conflict in Ukraine could also trigger a reconstruction boom in the country, serving as a tailwind for recovery in the Eurozone.

The USD strengthened following Donald Trump’s victory in the US presidential elections, amid market expectations of a ‘red wave’ in Congress. The anticipated second Trump administration is expected to implement aggressive fiscal and trade policies that could enhance the likelihood of a soft landing in the US and make US inflation more persistent. We, along with the US rates markets, expect that the Trump policy mix could shorten the Fed's easing cycle, which has already increased the USD's appeal across the board. Regarding the USD outlook, we believe that many positive factors are already priced into the currency, and we expect it to remain near recent highs but not surpass them on a sustained basis through 2025. While we cannot rule out further USD gains due to US tariffs, the timing and intensity of these measures remain uncertain. In the long run, we also think that a return to President Trump’s ‘Weak USD Doctrine’ and concerns about the Fed’s independence could put downward pressure on the USD as we approach 2026.

Increasing struggles in the Eurozone have driven safe-haven demand for the CHF, which may remain sought after until uncertainties are largely resolved. Assuming no lingering shocks, the CHF could revert to being a preferred funding currency due to the potential return of near-zero interest rates and its high valuation, while the SNB will likely monitor FX developments and Swiss disinflation closely.

Among the G10 currencies, the JPY was one of the least affected by tariffs during Trump’s first term. We expect the US-Japan rates spread to continue to narrow as the Fed cuts rates and the BoJ raises them further. This compression of the US-Japan spread will diminish the carry appeal of holding long positions in USD/JPY, while the exchange rate’s volatility is expected to remain high due to uncertainties surrounding the rate paths of the Fed and BoJ, as well as Trump’s policy agenda, particularly regarding trade. Japan’s Ministry of Finance will also likely be prepared to intervene to support the JPY.

FX investors should continue to view the GBP as a higher-yielding, safe-haven alternative to the EUR in 2024. This is due to the relative political stability and economic outperformance of the UK compared to the Eurozone. We observe that UK domestic demand has responded more positively to recent BoE easing than Eurozone domestic demand has to recent ECB rate cuts. This could support market expectations that the BoE will require a less aggressive easing cycle than the ECB to stimulate growth. Consequently, we are more optimistic about the GBP against the EUR and have lowered our EUR/GBP forecasts for 2025 and 2026. However, similar to EUR/USD, we have also downgraded our GBP/USD outlook following the US election, albeit to a lesser extent. We anticipate a more robust recovery in 2026.

Trump’s tariff threats have pushed USD/CAD to new highs above 1.40, but regardless of the incoming US administration's policy stance, risks to the CAD appear to be skewed to the downside in early 2025 due to a potentially widening gap between the BoC and Fed. However, the prospects of Canada outperforming the US in terms of growth could facilitate a gradual recovery for the CAD.

AUD/USD weakened during Trump’s first term due to his tariffs on China and a declining Australian-US rates differential. We expect Trump to be open to negotiations regarding his China tariffs, which may end up being less than the 60% he promised during his campaign, thereby supporting AUD/USD. Additionally, the RBA is likely to refrain from cutting rates while the Fed continues to lower its policy rate, which could mean the RBA misses this rate-cutting cycle entirely.

We have updated our XAU forecasts but maintain a downward trajectory for most of 2025. We anticipate a potential resurgence in gold prices into 2026, driven by growing market concerns regarding Fed independence and the threat of fiscal dominance in the US.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 71% and 74% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!