Daily Market Outlook, March 14, 2024

Daily Market Outlook, March 14, 2024

Munnelly’s Macro Minute…

“Markets Await Last Pieces Of The Data Puzzle Ahead Of Next Week's FOMC Meeting”

In response to mixed signals from global markets, Asian stock markets are also experiencing mixed trading on Thursday. Traders are exercising caution and staying on the sidelines as they await key U.S. retail sales, producer price inflation, and weekly jobless claims data later in the day, which could provide further insight into the outlook for interest rates. Although consumer inflation was slightly higher than expected, there remains optimism that the US Fed will reduce interest rates in June. The upcoming monetary policy meeting on March 19 and 20 will be closely monitored for any indications of potential timing for a rate cut. Continuing its decline from the last three sessions, the Japanese market is slightly down in volatile trading on Thursday, in response to the mixed signals from global markets overnight. The Nikkei 225 is approaching the 38.6k handle.

The overnight release of the RICS residential market survey offered further indication of improving sentiment in the UK housing market. The survey reported a net balance of estate agents indicating higher house prices at -10% in February, compared to -19% the previous month. Though still negative, this marks the sixth consecutive monthly rise. Additionally, the survey showed a positive net balance of 6% for new buyer enquiries, unchanged from last month and the joint highest in two years.

Today, there are no other major UK data releases on the docket, with attention shifting to this afternoon's US data and several ECB speakers scheduled throughout the day,while a first ECB rate cut in April has not been entirely dismissed, indications point towards June being the more probable option. This timing would afford policymakers additional data about the economy, including Q1 wage data, enabling a more informed decision-making process. Economic growth resilience and inflation prospects remain the focal points for Fed policymakers as well they deliberate on when to initiate interest rate cuts. Earlier this week, February CPI inflation data came in with a 0.4% month-on-month rise in the core measure (excluding energy and food), surpassing consensus expectations for the second consecutive month. Unexpectedly, the year-on-year comparison saw headline CPI rising to 3.2% from 3.1%. Today's producer price inflation data will offer insights into pipeline price pressures, look for an above-consensus month-on-month rise of 0.4% for the core measure.

Markets will also seek signs of a rebound in US economic activity following a generally weak start to the year attributed to temporary weather conditions and residual seasonal adjustment issues. Look for US retail sales to recover in February following a downside surprise in January, with a potential 0.7% month-on-month increase in headline retail sales, driven by higher auto sales and gasoline prices, alongside a 0.5% month-on-month rise in the core 'control group' measure, indicating a pickup in high-street sales. Overall it looks like US inflation and activity data will support delaying the first Fed rate cut until the middle of the year.

Overnight Newswire Updates of Note

Treasury’s Yellen: Rates ‘Unlikely’ To Return To Pre-Covid Levels

US To Impose New Sanctions On Occupied West Bank Outposts

BoJ Set To Discuss Negative Rate Exit As Japan Pay Raises Grow

BoJ Rate Hike Risk Revs Fiscal Reform Need, LDP Official Warns

BoJ To Go Slow In Hiking Rates, Says Ex-Central Bank Executive

Australia Pledges Cost-Of-Living Relief While Aiming For Surplus

UK Housing Market Sees More Buyers & Sellers As Prices Steady

Oil Holds Biggest Gains In Five Weeks As US Stockpiles Declined

Europe Regulator Says It Would Pull Boeing Approval If Needed

Altria Seeking To Sell More Than $2Bln Of Its AB InBev Shares

(Sourced from Bloomberg, Reuters and other reliable financial news outlets)

FX Options Expiries For 10am New York Cut

(1BLN+ represent larger expiries, more magnetic when trading within daily ATR)

EUR/USD: 1.0530 (EU1.16b), 1.0700 (EU760.8m), 1.0740 (EU754.1m)

USD/JPY: 147.00 ($2.56b), 153.00 ($1.94b), 151.00 ($1.24b)

USD/CNY: 7.2500 ($2.31b), 7.0600 ($1b), 7.2400 ($991.7m)

AUD/USD: 0.6275 (AUD1.14b), 0.6280 (AUD1.1b), 0.6480 (AUD1.08b)

USD/CAD: 1.3395 ($610m), 1.2915 ($528m), 1.3275 ($500m)

GBP/USD: 1.2550 (GBP1.02b), 1.2900 (GBP744.2m), 1.2350 (GBP661m)

NZD/USD: 0.6185 (NZD730.8m), 0.6080 (NZD540.8m), 0.6280 (NZD366.2m)

USD/BRL: 5.0000 ($897.4m), 4.9500 ($635m)

EUR/GBP: 0.8700 (EU400m)

USD/MXN: 16.50 ($300m)

The MOF data for the week-ended March 9 showed interesting moves and flows. Japanese investors bought a net of Y1.5796 trillion in foreign bonds, following Y490.1 billion in buys the previous week, as well as a paltry net of Y6.6 billion in bill buys. However, they continued to sell foreign stocks, with a net of Y661.5 billion sold. It seems that some Japanese investors repatriated their investments in favour of domestic stocks. On the other side, foreign investors were good buyers of Japanese assets, purchasing a net of Y376.6 billion in stocks, Y1.1526 trillion in JGBs, and Y2.2155 trillion in Japanese bills. The Japanese stock buys last week were not surprising, but net sales are likely this week. The buys of JGBs and Japanese bills suggest a move against the BOJ's March policy.

CFTC Data As Of 8/03/24

Bitcoin net short position is -1,352 contracts

Euro net long position is 66,311 contracts

Japanese Yen net short position is -118,843 contracts

Swiss Franc posts net short position of -17,551 contracts

British Pound net long position is 58,385 contracts

Equity fund managers cut S&P 500 CME net long position by 24,150 contracts to 917,973

Equity fund speculators trim S&P 500 CME net short position by 31,617 contracts to 402,895

Technical & Trade Views

SP500 Bullish Above Bearish Below 5150

Daily VWAP bullish

Weekly VWAP bullish

Below 5150 opens 5090

Primary support 5090

Primary objective is 5220

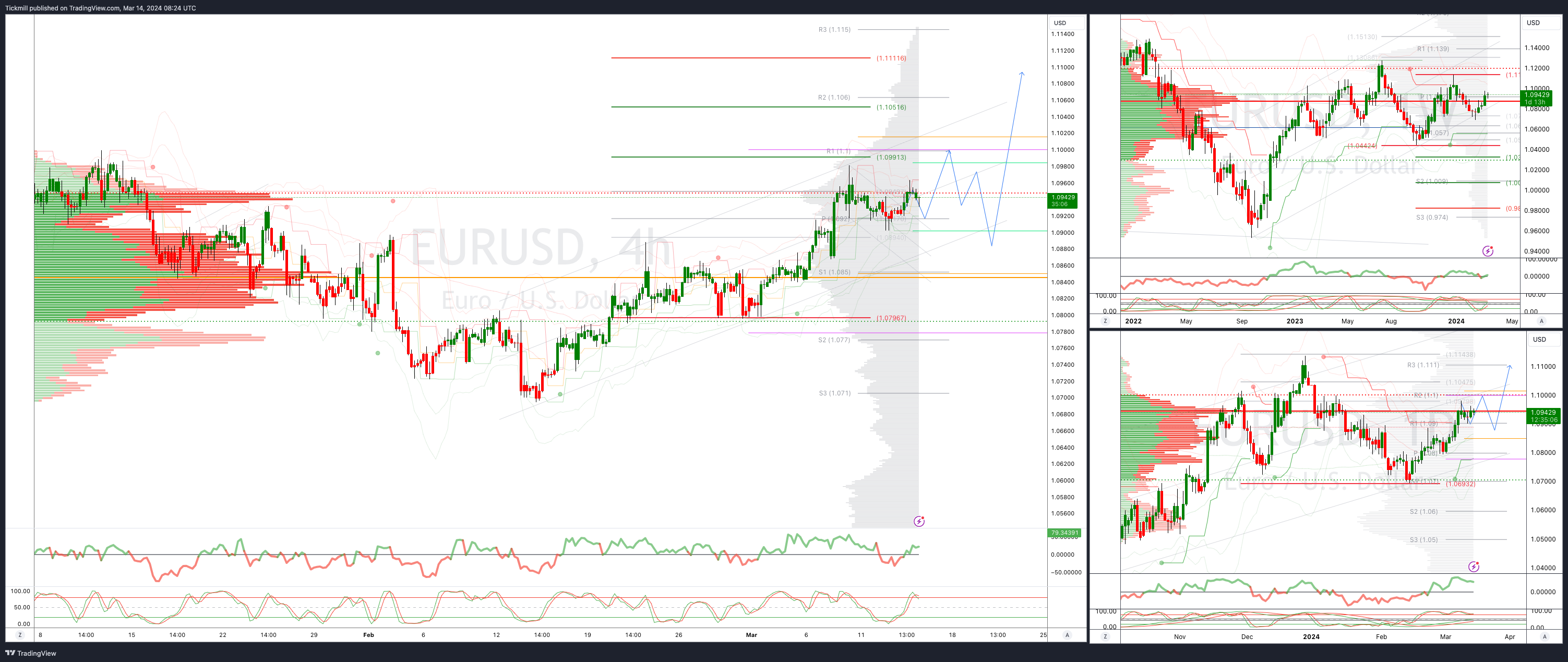

EURUSD Bullish Above Bearish Below 1.09

Daily VWAP bullish

Weekly VWAP bullish

Below 1.09 opens 1.0850

Primary support 1.08

Primary objective is 1.10

GBPUSD Bullish Above Bearish Below 1.2770

Daily VWAP bearish

Weekly VWAP bullish

Below 1.2750 opens 1.2700

Primary support is 1.2740

Primary objective 1.29

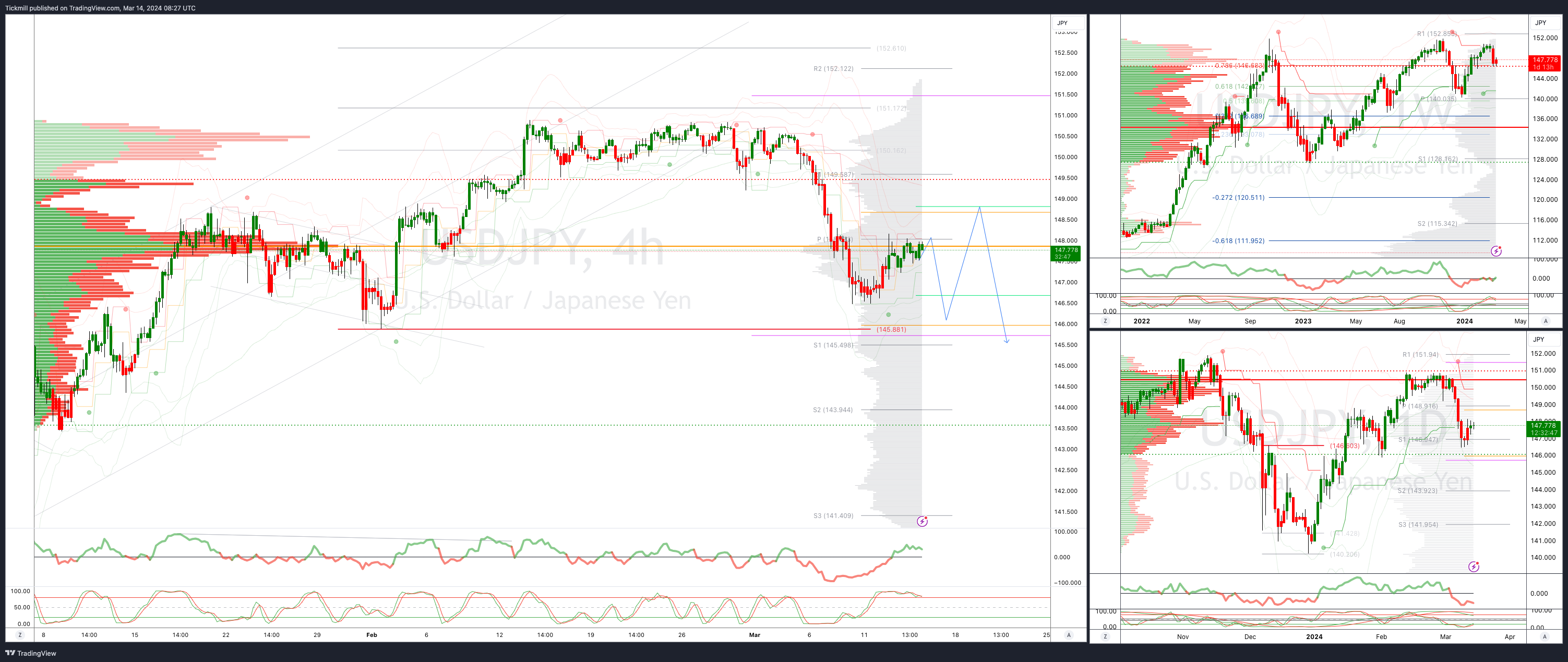

USDJPY Bullish Above Bearish Below 147.50

Daily VWAP bearish

Weekly VWAP bearish

Below 147.50 opens 145.88

Primary support 145.85

Primary objective is 152

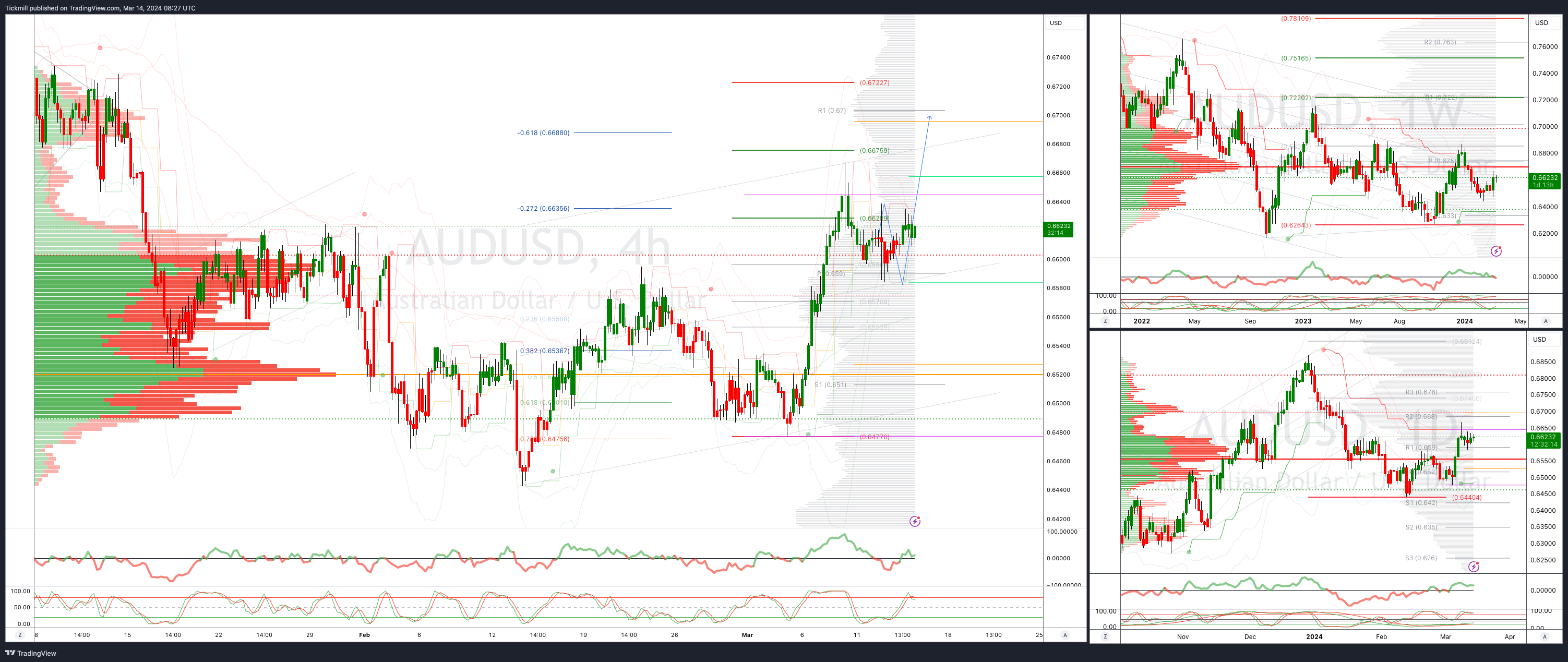

AUDUSD Bullish Above Bearish Below .6600

Daily VWAP bullish

Weekly VWAP bullish

Above .6640 opens .6700

Primary support .6477

Primary objective is .6700

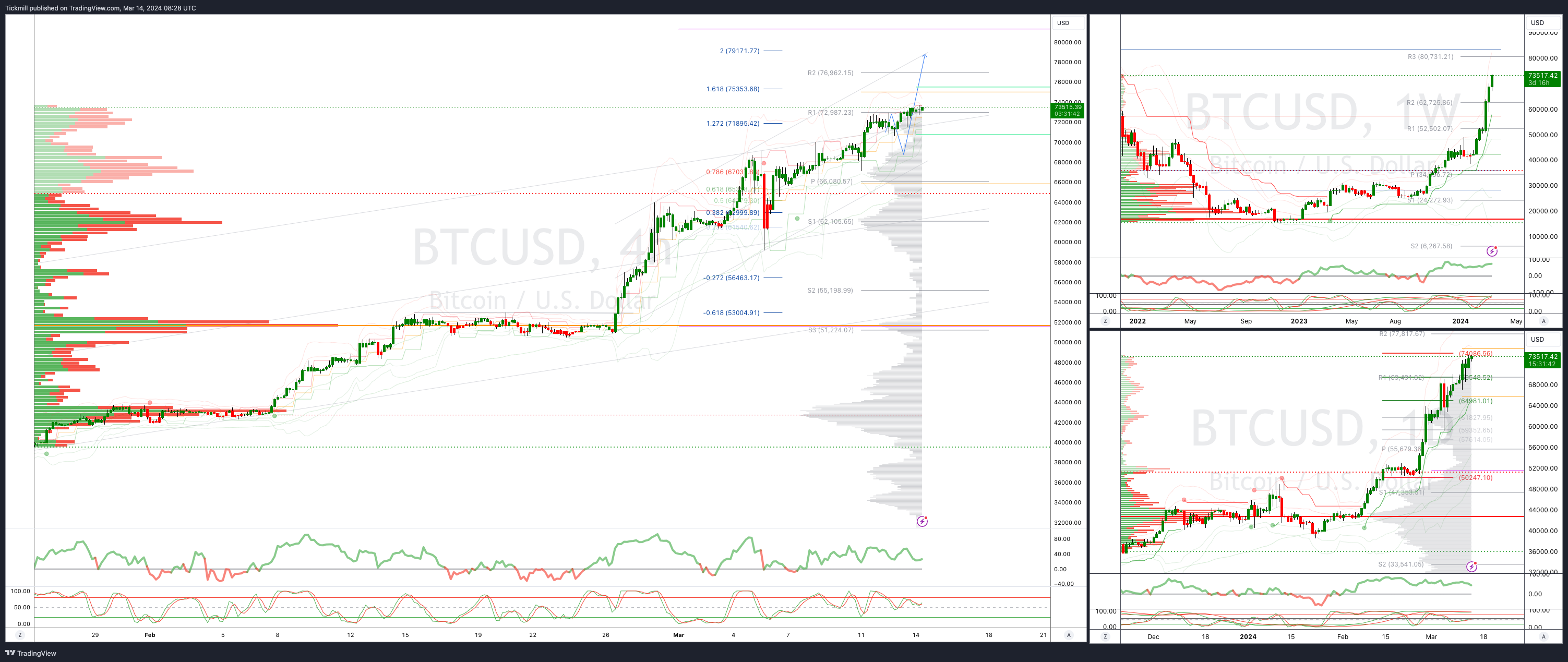

BTCUSD Bullish Above Bearish below 68000

Daily VWAP bullish

Weekly VWAP bullish

Below 66000 opens 62000

Primary support is 52800

Primary objective is 78000

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!