Daily Market Outlook, February 22, 2024

Daily Market Outlook, February 22, 2024

Munnelly’s Market Minute…

“Nvidia & The AI Tipping Point Sees Risk Sentiment Soar”

Most markets in the Asian region saw gains, driven by the positive performance of US tech futures following NVIDIA's blowout earnings referencing a tipping point in the global AI boom. The Nikkei 225 performed well, reaching new intraday record highs above 39,000, supported by strength in the tech sector. The KOSPI edged higher after the Bank of Korea decided to keep rates unchanged and suggested that a rate cut was unlikely in the near future. Both the Hang Seng and Shanghai Composite also saw gains, although there was choppy trading in Hong Kong due to US-China chip-related tensions, while mainland China remained stable following efforts to maintain stability.

Sensational headlines proclaiming a 'recession' filled the UK media last week following the Office for National Statistics' disclosure of a second consecutive quarter of negative growth in Q4. Nonetheless, Bank of England policymakers dismissed this particular recession label as 'unhelpful,' citing the enduring strength of the labor market. Governor Bailey remarked that the economy might have already emerged from the mild recession.

The anticipated UK flash PMIs for February are poised to indicate expansion (above a 50 reading) for a fourth consecutive month, with the composite index gaining momentum since late 2023, mainly driven by a surge in the services index. Markets expect this trend to persist in February, projecting a further increase in the services measure to 55.5 from 54.3, marking its highest level since last April. Conversely, the manufacturing index remains below 50, signaling contracting activity. It is expected this trend will continue in February, signs of stabilization in the sector may emerge, with the headline measure forecasted to rise to its highest level since last April. The PMI data will also be scrutinized for indications of supply chain strain due to ongoing issues in the Red Sea. Recent signals suggest that after an initial lengthening in delivery times and a consequent rise in shipping costs, the situation has stabilized; it will be intriguing to observe if the data confirm this. Additionally, the latest GfK consumer confidence report is scheduled for release early Friday. Look for a fourth consecutive increase to -18, its highest since the end of 2021, reflecting households' growing confidence in both their personal situations and the overall economy.

Eurozone and US flash PMIs are also set for release today. PMI data in the Eurozone have been less optimistic than in the UK, with the composite index remaining below 50 for the eighth consecutive month in January. While both the manufacturing and services indices are also below 50, they have been inching upwards, look for a similar trend in February, suggesting tentative signs of economic improvement. The US PMI may garner more attention than usual given the relatively quiet data week. January readings indicated continued economic growth primarily fueled by services, and it looks like a similar scenario in February is likely. The Federal Reserve's Vice Chair Jefferson, along with Governors Bowman and Cook, who are all voters, are scheduled to give speeches, as well as the 2026 voters Harker and Kashkari.

Overnight Newswire Updates of Note

Fed Minutes Show Unease Over Premature Interest Rate Cuts

Nvidia Revenue Reach New Heights, Forecasts Bigger AI Boom

Fed’s Bowman Says That Time For Rate Cut Certainly Not Now

House GOP Hardliners Ask Johnson To Abandon Spending Talks

Poll: BoJ To Scrap Negative Interest Rates In April, Say Over 80%

Japanese Manufacturing PMI Falls To Lowest Since August 2020

Bond Traders Prepare For Another US Selloff, Unwind Bullish Bets

Oil Holds Gain As Signs Of Tight Market Offsets Demand Concerns

Japanese Stock Market Passes Record Closing Level After 34 Years

(Sourced from Bloomberg, Reuters and other reliable financial news outlets)

FX Options Expiries For 10am New York Cut

(1BLN+ represent larger expiries, more magnetic when trading within daily ATR)

EUR/USD: 1.0770 (EU731.6m), 1.0425 (EU654m), 1.0905 (EU652.9m)

USD/JPY: 145.00 ($648m), 138.00 ($440m), 149.00 ($434.7m)

AUD/USD: 0.6350 (AUD585.5m)

USD/CNY: 7.4000 ($1.15b)f 7.2250 ($839.9m), 7.1870 ($825.7m)

USD/CAD: 1.3500 ($930m), 1.3470 ($538.6m)

GBP/USD: 1.2803 (GBP703m), 1.1958 (GBP500m), 1.3550 (GBP376.4m)

NZD/USD: 0.6030 (NZD750m), 0.6150 (NZD549.2m), 0.5974 (NZD353.2m)

USD/BRL: 4.9500 ($956.6m)

EUR/GBP: 0.8450 (EU400m)

CFTC Data As Of 13/02/24

British Pound net long position is 50,472 contracts.

Japanese Yen net short position is -111,536 contracts.

Bitcoin net short position is -1,921 contracts.

Swiss Franc posts net short position of -6,014 contracts.

Japanese Yen net short position is -111,536 contracts.

Equity Fund managers raise S&P 500 CME net long position by 17.391 contracts to 930,253.

Equity fund speculators trim S&P 500 CME net short position by 39.481 contracts to 384.474.

Technical & Trade Views

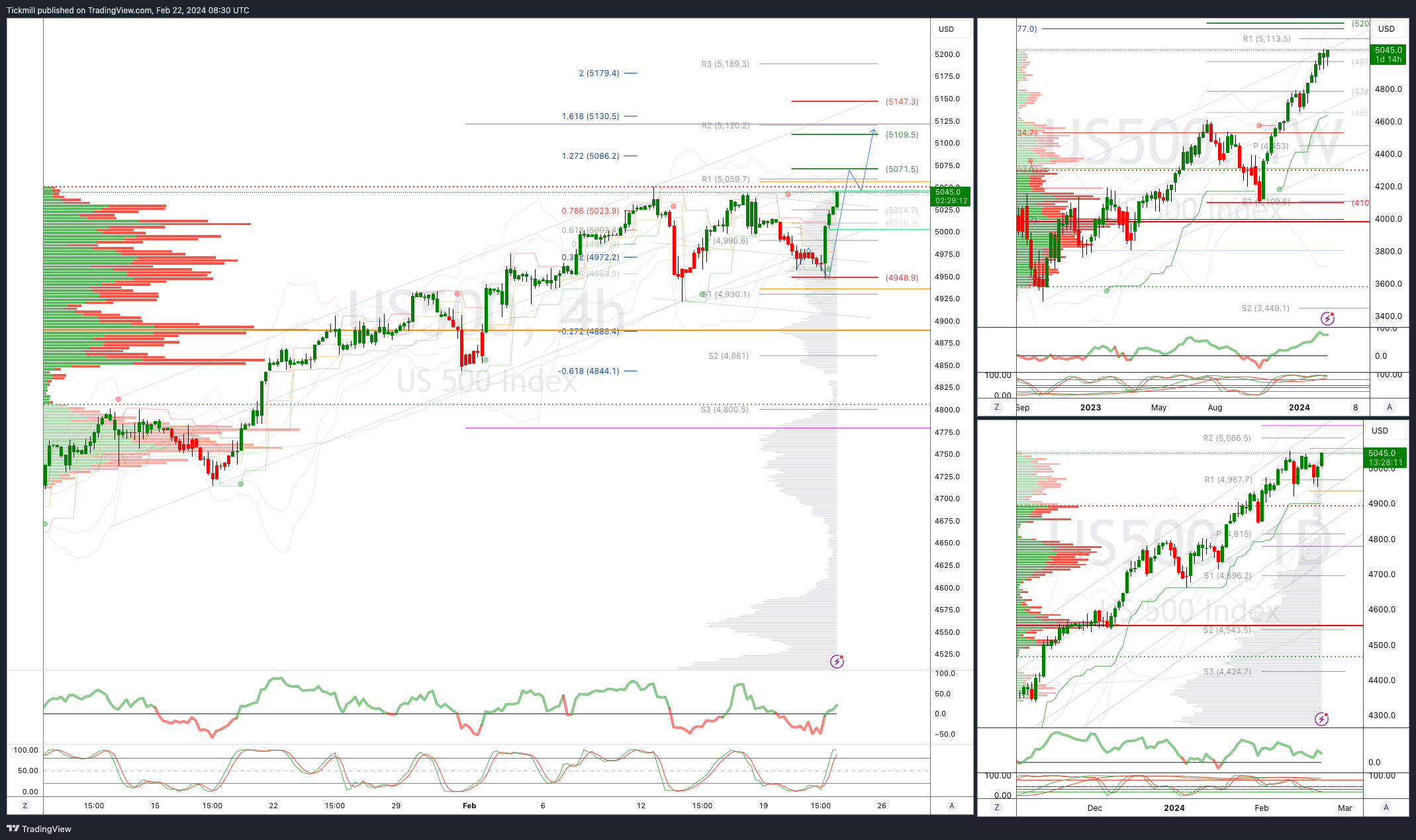

SP500 Bullish Above Bearish Below 5025

Daily VWAP bullish

Weekly VWAP bullish

Above 5045 opens 5086

Primary support 4900

Primary objective is 5120

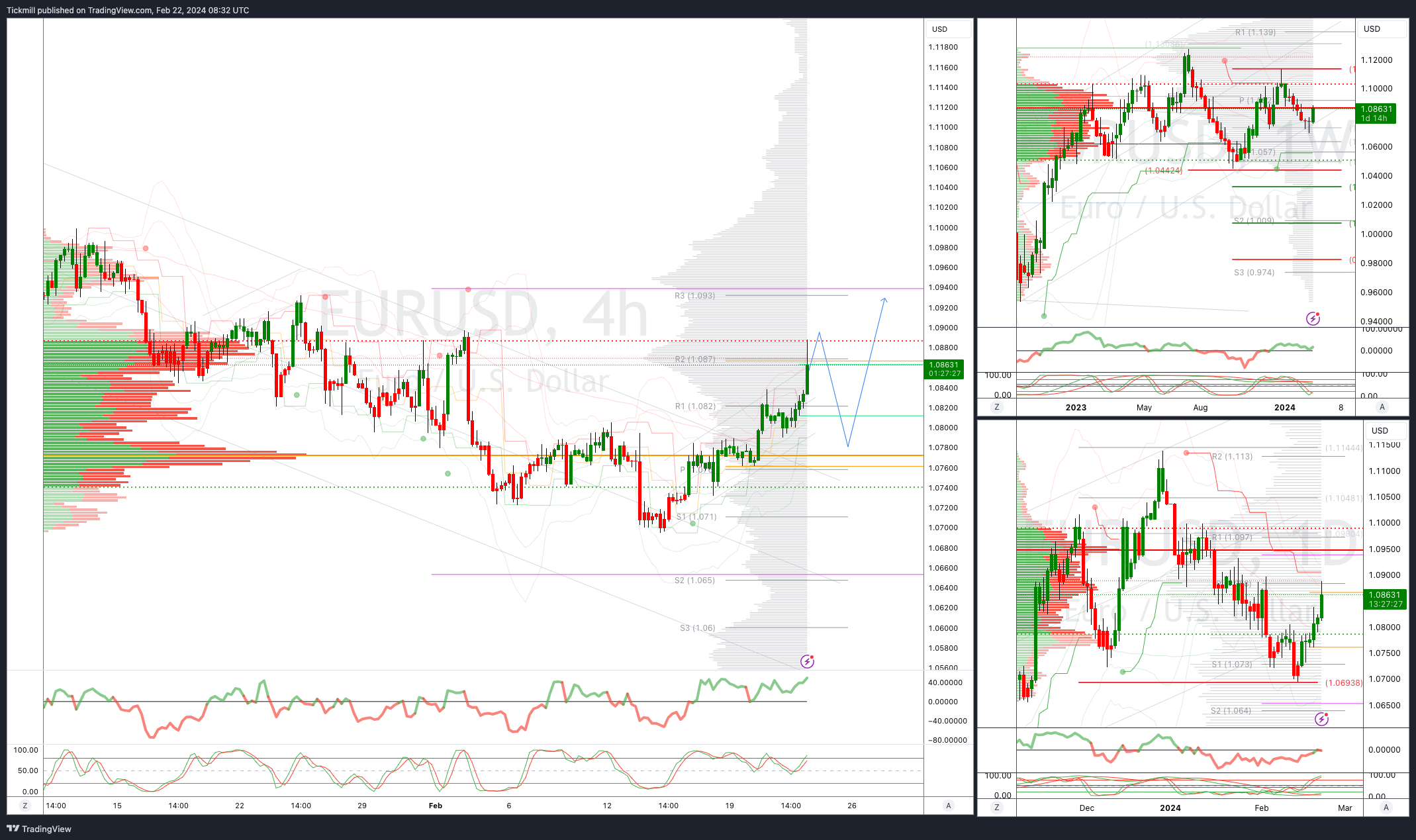

EURUSD Bullish Above Bearish Below 1.08

Daily VWAP bullish

Weekly VWAP bullish

Above 1.109 opens 1.10

Primary resistance 1.0950

Primary objective is 1.0950

GBPUSD Bullish Above Bearish Below 1.2683

Daily VWAP bullish

Weekly VWAP bullish

Above 1.27 opens 1.2770

Primary resistance is 1.2785

Primary objective 1.2830

USDJPY Bullish Above Bearish Below 149.50

Daily VWAP bullish

Weekly VWAP bullish

Below 149.50 opens 148.70

Primary support 145.85

Primary objective is 152

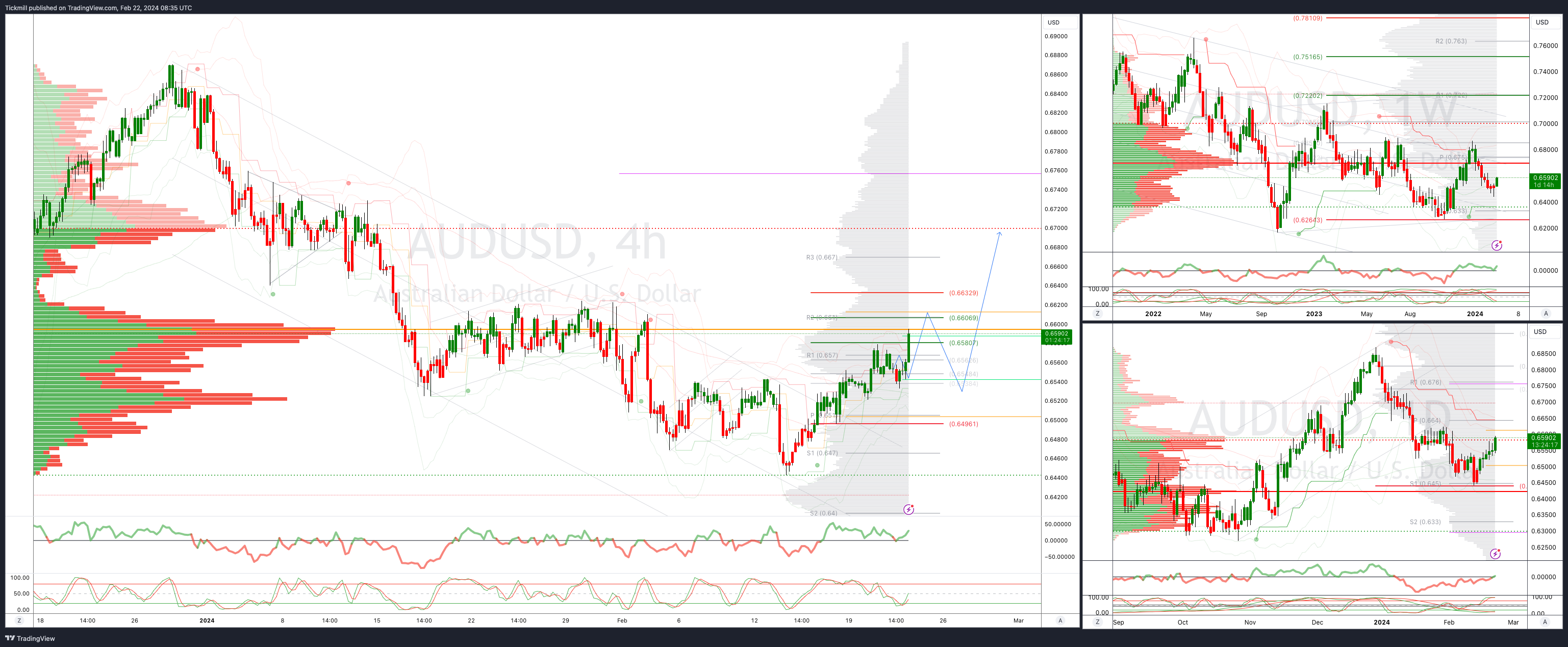

AUDUSD Bullish Above Bearish Below .6590

Daily VWAP bullish

Weekly VWAP bearish

Below .6500 opens .6420

Primary support .6525

Primary objective is .6700

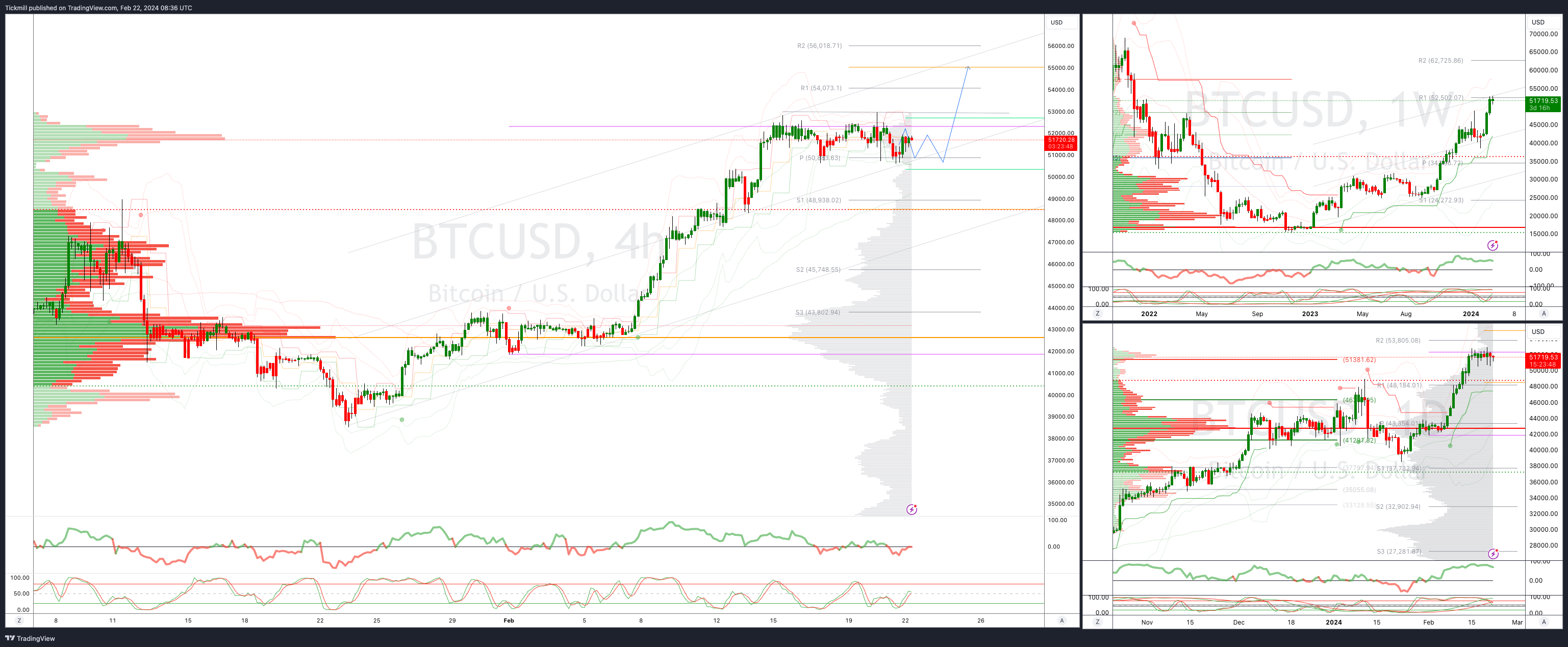

BTCUSD Bullish Above Bearish below 51000

Daily VWAP bullish

Weekly VWAP bullish

Below 48500 opens 46500

Primary support is 44390

Primary objective is 54000

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!